I’ve been on Zepbound for a while now. I have a doctor, a prescription, and insurance that covers it, so my own access path is straightforward. Most weeks I forget that the path I took is one of five, and that the path you take might shape the cost more than the drug itself does.

The Lilly news this week put that in sharp relief. CVS Caremark announced on May 28, 2026, that it was restoring Zepbound to its standard commercial formulary and adding Foundayo, Lilly’s new oral GLP-1, on top of it. Lilly stock jumped enough to push the company past a $1 trillion market cap, the first pharma company ever to hit that line. The decision that triggered all of it came from one company. Not Lilly, not Novo, not the FDA. A pharmacy benefit manager.

If you read coverage of these drugs you’ve probably heard “PBM” mentioned and maybe not really understood what it actually means or why it matters. The short version is that for most Americans, a PBM decides whether your insurance pays for Zepbound or Mounjaro, what tier it lands on, and what hurdles you go through before the script gets filled. The Lilly trillion-dollar moment was a PBM moment.

So here are the five channels Americans actually use to get tirzepatide, the molecule behind both Zepbound and Mounjaro. They overlap in places, they don’t cost the same, and the one you end up on says more about your employer and your zip code than about your motivation.

Your insurance company doesn’t decide. Three companies you’ve never met do.

Get the next one in your inbox

I cover the GLP-1 access changes and the rest of this beat weekly. Free, no spam, unsubscribe whenever.

If you have employer-based health insurance and your plan covers tirzepatide for weight loss, the company that approved that coverage probably isn’t your insurance company. It’s the pharmacy benefit manager your insurance company hired.

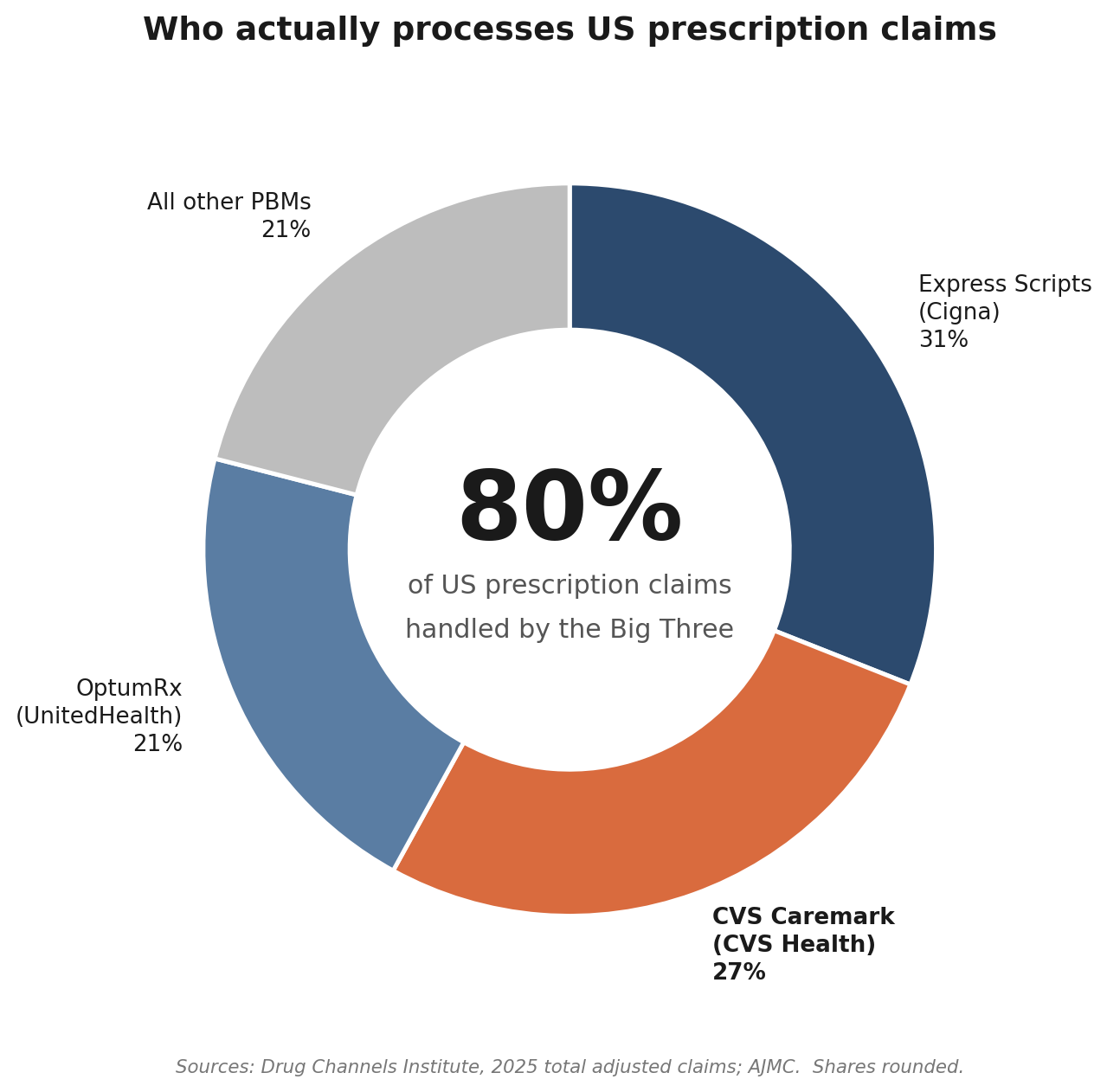

Three PBMs handle roughly 80% of US prescription claims. Express Scripts, owned by Cigna, processed about 2.2 billion adjusted prescription claims in 2025 and is currently the largest. CVS Caremark, owned by CVS Health, came in just behind at about 1.9 billion. OptumRx, owned by UnitedHealth, rounds out the Big Three. Between them, they’re the gatekeepers for the prescription benefits of more than 200 million Americans.

A PBM does several things that overlap with what most people assume their insurer does. It negotiates with drug manufacturers over rebates. It builds a formulary, the list of drugs your plan covers and at what tier. It runs the network of pharmacies that fill scripts under your plan. And it handles utilization management, the system of prior authorizations and step therapy that decides whether a particular script for a particular patient actually goes through.

Manufacturers compete on rebate. To get a drug onto a PBM’s preferred tier, the manufacturer agrees to pay a discount on every prescription that runs through that PBM. Sometimes the rebate is a straightforward dollar discount, sometimes it’s bundled into a contract covering multiple drugs, sometimes it carries volume thresholds. The contracts are confidential. The patient-facing copay is loosely related to the negotiated rebate but isn’t the same number.

This is why a single PBM decision can move a trillion-dollar stock. When CVS Caremark added Wegovy as the preferred GLP-1 last year and dropped Zepbound, Lilly lost preferred access to about 25 to 30 million plan members on the Caremark standard commercial template overnight. When Caremark restored Zepbound and added Foundayo on May 28, 2026, Lilly got it back. Same template, same members. The drug didn’t change. The contract did.

Plan sponsors complicate this further. Most employers and health plans use a PBM’s standard template as a starting point and then customize. So even if Zepbound is on CVS Caremark’s preferred list as of October 1, 2026, your specific employer plan can choose to exclude weight-loss GLP-1s entirely. Plenty do. The CVS press release uses the phrase “where approved for coverage by plans” deliberately.

In practice, my insurer wasn’t the decider. The PBM set the template, and my employer picked the rules. Any one of those three can block a script.

Commercial insurance is the front door, and it just shifted.

For most working-age adults, the first stop is commercial insurance through an employer. The reach is huge. Around 165 million Americans have employer-sponsored health coverage, plus another 24 million on individual market plans. The bulk of GLP-1 access still runs through this channel.

What that access looks like has changed twice in the last twelve months, both times because of one PBM.

In May 2025, CVS Caremark struck a deal with Novo Nordisk that made Wegovy the preferred weight-loss GLP-1 on its standard commercial formulary template and dropped Zepbound. Around 25 to 30 million Americans whose plans used that template were affected. People who had been on Zepbound either switched, paid more out of pocket, jumped through prior-authorization hoops, or stopped.

In May 2026, the same PBM reversed course. Effective June 1, 2026, the new-to-market block on Lilly’s oral pill Foundayo lifts. Effective October 1, 2026, Zepbound returns as a preferred option. Wegovy and the Wegovy pill keep their preferred status, so both manufacturers now sit side by side on the same template. The earlier deal isn’t replaced. It’s expanded.

Express Scripts and OptumRx run their own contracts. Express Scripts has its own formulary template, currently with Zepbound and Wegovy both in preferred status under different rebate structures. OptumRx historically has been more permissive on GLP-1 weight-loss coverage than Caremark was last year. None of these contracts are public in detail. What you see is the formulary, which your plan sponsor either adopts or customizes.

If you’re covered through work, do a quick sanity check: who runs your pharmacy benefits, what your formulary says about Zepbound, Mounjaro, Wegovy, and Foundayo, and whether your employer excluded weight-loss GLP-1s at the plan-design level. The benefits portal usually answers all three in a few minutes.

The benefits portal is usually the fastest answer. Sometimes the formulary lookup tool surfaces the tier and the prior-authorization criteria. Sometimes it just shows “covered” or “not covered” without the fine print. Calling the number on the back of your insurance card and asking for a benefits coordinator works too, and they can usually tell you the prior-authorization criteria your plan requires.

Prior authorization is the second hurdle even when the drug is covered. The typical criteria are BMI of 30 or higher, or BMI of 27 with at least one comorbidity like hypertension or sleep apnea. Some plans require documented prior weight-loss attempts. Some require step therapy through an older or cheaper medication first. All of this happens between your doctor and the PBM, not between you and your insurer.

If your plan covers Mounjaro for diabetes and you have type 2 diabetes, you’re on a different track entirely. Mounjaro is the same molecule as Zepbound, tirzepatide, but the on-label diabetes indication makes coverage substantially easier almost everywhere. People who qualify for both occasionally take the diabetes path because the path of less resistance is the path that gets the script filled.

Medicare just opened a window. Medicaid varies by zip code.

The Medicare story is going to change for one specific group on July 1, 2026, and stay the same for most beneficiaries.

The default rule for Medicare Part D since 2003 has been that drugs used for weight loss are excluded by statute. That excluded Wegovy and Zepbound from default Part D coverage even when the patient had obesity that everyone agreed was a medical problem. People aged 65 and older mostly had to find another channel, and most of them did so by paying cash.

CMS announced earlier in 2026 that it would use existing regulatory authority to bridge that gap for a defined window. From July 1, 2026 through December 31, 2027, Medicare Part D and Medicare Advantage plans can cover Wegovy, Zepbound, and Foundayo for adults with obesity, with a monthly copay around $50 for eligible patients. The eligibility criteria are tighter than commercial-plan PA rules in some places and looser in others. BMI of 35 or higher with no further requirement. BMI of 30 with heart failure, controlled hypertension on two or more medications, or chronic kidney disease stage 3a or above. BMI of 27 with prior heart attack, prior stroke, symptomatic peripheral artery disease, or pre-diabetes per ADA criteria.

I wrote up the eligibility logic and the prior-authorization checklist in detail at my Medicare GLP-1 bridge post. The short version is that it’s the most affordable channel for people who qualify, and it ends on December 31, 2027 unless CMS extends it.

The bridge only covers people who are enrolled in Medicare Part D or in a Medicare Advantage plan that includes Part D. Original Medicare without a Part D plan doesn’t qualify. The bridge requires you to be prescribed alongside structured nutrition and physical activity, which most prescribers handle by documenting it in the chart but isn’t fully self-evident. And Medicare Advantage formularies can still impose plan-level utilization management on top of the bridge, so the actual experience varies by plan.

Medicaid is a separate story and a state-by-state one. Some states cover Zepbound and Wegovy for obesity through their managed-care plans. Some cover only the diabetes indication of Mounjaro and Ozempic. Some require BMI thresholds higher than the FDA label. Some require step therapy through a bariatric surgery referral first, which is a remarkable bar in practice. The map shifts every legislative session. If you’re on Medicaid, the answer is to call your specific plan or check the state Medicaid pharmacy benefit page. There is no shortcut here.

Self-pay from the manufacturer is the new normal.

A year ago, the self-pay landscape for these drugs was list price or nothing. Zepbound at $1,000 a month and up out of pocket. Wegovy similar. Almost nobody paid those numbers, because almost nobody was actually paying full list. The patients who didn’t have coverage either paid retail and got a partial GoodRx discount, or they went to compounding.

That changed in mid-2025 and continued through 2026 as both manufacturers built direct-to-patient programs.

Lilly runs LillyDirect for Zepbound. The Self Pay Journey Program announced in February 2026 prices the single-dose vials at $299 a month for 2.5 mg, $399 for 5 mg, and $449 a month flat for any of the higher doses from 7.5 mg through 15 mg. The vials require drawing the medication with a syringe, which is a step the pen format skipped, and you have to refill within 45 days of your prior shipment to hold the $449 price at the higher doses. Miss the window and you pay the standard self-pay price, which climbs back toward $1,000 a month at the top dose.

Novo runs NovoCare for Wegovy. Through the first half of 2026 the entry-level offer was $199 a month for the lower doses for new patients, with a two-month limit before pricing reverts to $349 a month for most of the dose ladder and $399 for the new high-dose 7.2 mg pen. The new Wegovy pill is priced at $149 a month for the 1.5 mg and 4 mg tablets through their respective promotional windows.

Foundayo, the new oral GLP-1 from Lilly, launched at roughly $349 a month on direct self-pay through LillyDirect, with the same prescriber requirements as Zepbound.

There’s also Amazon Pharmacy in the mix as of May 2026. The Ozempic pill is stocked at Amazon kiosks for $149 a month cash or $25 a month with insurance at qualifying retail sites. Amazon’s network is expanding from about 3,000 locations to 4,500 by the end of 2026. This is the same Ozempic pill that Novo rebranded earlier this year from its diabetes line.

GoodRx is worth mentioning because most readers know it and because it still has a role. For people who already have a Zepbound or Mounjaro prescription and want to see what the retail pharmacies in their area would charge with the coupon, GoodRx remains the fastest one-tab answer. It’s almost never going to beat LillyDirect or NovoCare on price for the brand-name pen or vial, but it can occasionally surface a useful discount, and for related drugs in the family it sometimes wins.

If I couldn’t get coverage tomorrow, I’d budget $300 to $450 a month and go direct through LillyDirect or NovoCare. That isn’t a workaround anymore. It’s the standard path for a lot of people, and it’s a different number than the $1,000 to $1,500 list prices that defined the landscape twelve months ago.

Compounded pharmacies and the gray market: cheaper, riskier, narrower than they used to be.

For two years, the cheapest legal-ish path to tirzepatide was compounded. When FDA placed tirzepatide on its official drug shortage list in late 2022, compounding pharmacies were allowed to make essentially copies of the drug for individual patients whose doctors had written prescriptions for it. Hundreds of thousands of Americans ended up on compounded tirzepatide, paying roughly $200 to $400 a month for a vial that arrived from a compounding pharmacy in Florida or Texas.

The legal framework split between two pharmacy types. 503A pharmacies prepare medications for individual identified patients with valid prescriptions. 503B outsourcing facilities make larger batches under more FDA oversight and supply directly to healthcare facilities. Both types could compound tirzepatide while it was on the shortage list, but the rules and inspection regimes were different.

That regulatory architecture started to crack in late 2024, when Lilly told FDA that tirzepatide was no longer in shortage. FDA agreed in March 2025, removed tirzepatide from the official shortage list, and gave compounders a wind-down period. The wind-down ended for 503A pharmacies in mid-2025 and for 503B facilities in late 2025. As of 2026, the legal carve-out is essentially gone.

Compounders still operate in this space, but the legal posture has shifted. Some claim a personalized-formulation justification under the 503A rules for adding B12 or other adjuncts. The FDA has signaled this is not a legitimate workaround. Some 503B facilities have shut their tirzepatide lines entirely, including a recent inspection-related stoppage at BPI Labs that lit up the compounded-tirzepatide subreddit in May 2026. That same month, FDA went a step further and proposed to keep semaglutide, tirzepatide, and liraglutide off its 503B bulks list entirely, finding no clinical need for outsourcing facilities to compound them from bulk ingredients, with the public comment period closing June 30. If that proposal is finalized, the last legal route for large-scale compounding of these drugs closes, since a substance that sits on neither the bulks list nor the shortage list can’t be compounded from bulk at all. The reality is that the compounded channel is smaller and riskier than it was a year ago, and the regulatory tide is running against it.

What’s left below that is the gray market. Peptide vendors selling for-research-use-only tirzepatide vials sourced from manufacturers overseas. Telegram channels. Lifter forums where people post their bloodwork after eight weeks on a vendor’s reta or tirz. Some of these vendors run COAs from independent labs, where the certificate confirms the molecule matches what’s on the label. Many don’t. The dose accuracy is variable. The identity of the active ingredient is sometimes wrong, which is its own kind of dangerous when you’re injecting yourself weekly.

I have a full post at Zepbound vs grey market tirzepatide that lays out the price math and the risk math side by side, and the conclusion I came to there hasn’t changed. At current self-pay prices from LillyDirect, the gray-market discount is no longer the 90% it was in 2023. It’s closer to 60% on average, with the difference paid in QC risk, dose risk, and the legal posture of importing or possessing a research chemical. For most readers, that math doesn’t pencil out unless the alternative is no medication at all.

The gray market is real and it isn’t going away. But it isn’t the same deal it was, and people who started on it in 2024 are increasingly switching back to the regulated channels now that LillyDirect and NovoCare have brought their self-pay prices into range.

What I’d do if I were starting tomorrow

If I were starting tomorrow with no medication and no clear path, I’d start with employer insurance and work down from there.

I’d start there even if I assumed the answer was no. The CVS announcement this week added Zepbound and Foundayo back to roughly 25 to 30 million people’s plan templates, and the actual coverage at the individual-plan level keeps shifting. The benefits portal takes ten minutes. The downside of skipping it is paying $300 a month I didn’t have to.

If commercial insurance wouldn’t pay, I’d go straight to LillyDirect for Zepbound vials at $299 to $449 a month, or NovoCare for Wegovy at $149 to $499 depending on dose and promo. With no coverage and a willingness to handle the syringe draw, that’s where the math works fastest.

If I were on Medicare and met the eligibility criteria, the bridge from July 1, 2026 through December 31, 2027 at around $50 a month is the cheapest channel that exists. I’d plan around it.

If cost was the genuine blocker and the manufacturer-direct numbers were still too high, I’d talk to my doctor about whether a compounding pharmacy is a legitimate option given the current regulatory posture. The honest answer is less than it used to be.

The gray market would be last, and only with eyes wide open and at least one or two layers of verification. I personally wouldn’t use it both for risk and ethical/legal reasons. Some readers will, and I get why.

I cover this beat every week. If you want a note when the rules change again, drop your email below. They will change.

I keep a running tracker of every GLP-1 and incretin drug, approved and still in the pipeline, with what each one targets, how far along it is, and what's coming next.

See the full GLP-1 Pipeline Tracker →About Gunnar

Gunnar is 53. He lost about 170 pounds, trains in a garage gym, and writes DadStrengthDaily from personal experience, citing primary sources where he can. He also moderates r/ProactiveHealth. He is not a doctor, and nothing here is medical advice. Talk to your own doctor before acting on anything, especially GLP-1s, TRT, blood pressure, sleep apnea, and cancer screening.